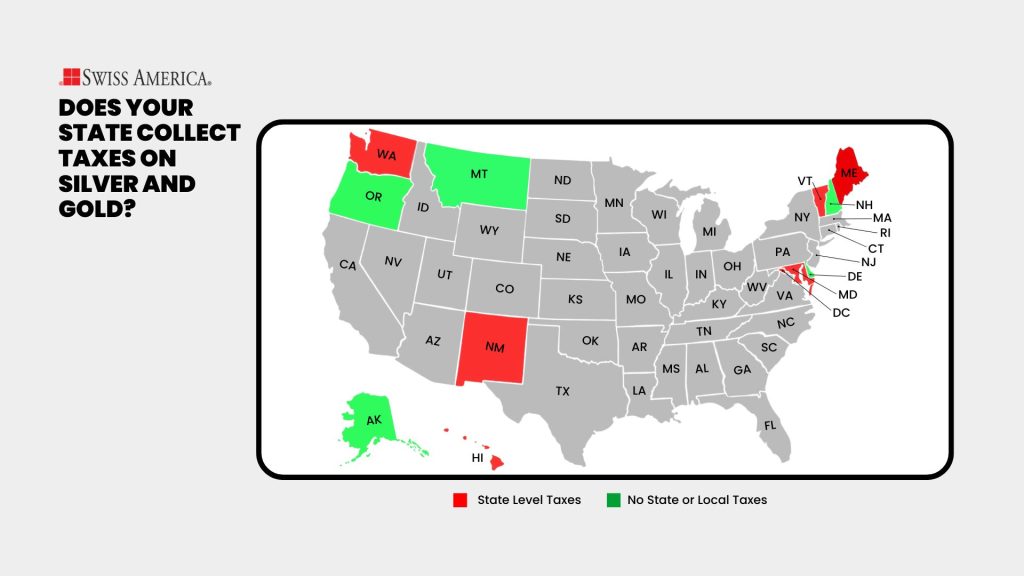

Sales tax on gold and silver by state comes down to where you live. As of 2026, 44 states exempt precious metals from state sales tax. Only Hawaii, Maine, Maryland, New Mexico, Vermont, and Washington still charge it, along with Washington, D.C.

Five states, Alaska, Delaware, Montana, New Hampshire, and Oregon, charge nothing at either the state or local level.

Which states have no sales tax on gold and silver?

As of 2026, 44 states exempt gold and silver bullion from state sales tax. Here is the quick breakdown:

- No state or local sales tax: Alaska, Delaware, Montana, New Hampshire, and Oregon charge nothing at either level.

- No state sales tax, local tax may apply: 39 states exempt precious metals at the state level but still allow county or city sales tax.

- Still charge state sales tax: Hawaii, Maine, Maryland, New Mexico, Vermont, and Washington, along with Washington, D.C.

Two changes drove the recent shifts. Maryland added a 6% sales tax on bullion under House Bill 352 in 2025. Washington followed with a 6.5% tax starting January 1, 2026. If you live in either state, your cost of buying gold has increased.

Overview of sales tax on precious metals

Two types of tax can apply when you purchase investment assets like gold or silver: state sales tax and local sales tax.

State sales tax

Most states do not charge state-level sales tax on precious metals. As of 2026, the states that do are Hawaii, Maine, Maryland, New Mexico, Vermont, and Washington. Washington, D.C., also applies sales tax to bullion purchases.

Local sales tax

Local sales tax is a separate layer. It applies in most states regardless of whether the state itself charges sales tax. The only places where you pay no local sales tax are Alaska, Delaware, Montana, New Hampshire, and Oregon.

If you live anywhere else, you will owe local tax even if your state exempts precious metals.

Free Resource

Want this sent to you?

Call us for a free precious metals kit — no obligation.

State-by-state analysis

Here is a summary of how states tax gold and silver purchases:

| Tax type | States |

| No state or local sales tax | Alaska, Delaware, Montana, New Hampshire, Oregon |

| No state sales tax on gold and silver | Alabama, Arizona, Arkansas, Colorado, Georgia, Idaho, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Michigan, Minnesota, Mississippi, Missouri, Nebraska, Nevada, New Jersey, North Carolina, North Dakota, Ohio, Oklahoma, Pennsylvania, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia, West Virginia, Wisconsin, Wyoming |

| Conditional or threshold-based tax | California, Connecticut, Florida, Massachusetts, New York |

| State sales tax | Hawaii, Maine, Maryland, New Mexico, Vermont, Washington, and Washington, D.C. |

The specific rules for each state include:

Alabama

No state sales tax on precious metals. Act 2018-164 created this exemption effective June 1, 2018. SB 13 in the 2022 session extended it five years, now running through May 31, 2028.

Local taxes: Yes

Alaska

No statewide sales tax on precious metals or any other purchases.

Local taxes: No

Arizona

No statewide sales tax on precious metals.

Local taxes: Yes

Arkansas

SB 336, effective October 1, 2021, exempts gold and silver bullion from sales tax. The state also made gold and silver legal tender, allowing residents to use bullion coins to pay for goods and services.

Local taxes: Yes

California

Under CDTFA Regulation 1599, California exempts bulk sales of gold or silver bullion of $2,000 or more in a single transaction, effective July 1, 2023. The exemption applies only when the sale is made by or through a person registered under the federal Commodity Exchange Act. Standard retail purchases below $2,000 are taxable, and purchases above $2,000 are taxable unless the seller meets that criterion.

Local taxes: Yes

Colorado

No state sales tax on precious metals. The exemption does not cover all numismatic coins, so check the state tax bulletin if you are buying collectibles.

Local taxes: Yes

Connecticut

Purchases under $1,000 are subject to a 6.35% state tax. Purchases of $1,000 or more are exempt.

Local taxes: Yes

Delaware

No state sales tax on any purchases, including precious metals.

Local taxes: No

Florida

No state sales tax on precious metals purchases above $500.

Local taxes: Yes

Georgia

No state sales tax on precious metals.

Local taxes: Yes

Hawaii

Hawaii applies a General Excise Tax of 4% to gold and silver bullion at the state level.

Local taxes: Yes

Idaho

State statute exempts gold and silver bullion from sales taxes.

Local taxes: Yes

Illinois

No statewide sales tax on bullion purchases.

Local taxes: Yes

Indiana

No sales tax on gold that qualifies for an IRA under IRS rules. U.S. legal tender coins are also exempt. Collectible coins or bullion outside these definitions may still be taxable.

Local taxes: Yes

Iowa

No state sales tax on precious metals. Iowa also eliminated capital gains tax on these investments under House File 659.

Local taxes: Yes

Kansas

House Bill 2140, passed in 2019, exempts precious metals from sales tax.

Local taxes: Yes

Kentucky

House Bill 8, passed in the 2024 Regular Session, created a sales tax exemption for gold and silver bullion, effective August 1, 2024.

Local taxes: Yes

Louisiana

The state recognizes gold and silver bullion as tangible personal property and exempts these purchases from sales tax.

Local taxes: Yes

Maine

Maine charges 5.5% sales tax on gold and silver bullion.

Local taxes: Yes

Maryland

House Bill 352 (the Budget Reconciliation and Financing Act of 2025) applies a 6% sales tax to gold and silver bullion as of July 1, 2025.

Local taxes: Yes

Massachusetts

Purchases over $1,000 are exempt from sales tax under state statute. Purchases below that amount are taxable.

Local taxes: Yes

Michigan

No sales tax on gold, silver, or platinum bullion at 90% purity or higher per state law.

Local taxes: Yes

Minnesota

No state sales tax on precious metals at 99.9% purity or higher.

Local taxes: Yes

Mississippi

Senate Bill 2862, passed in 2023, made precious metal purchases sales tax-exempt.

Local taxes: Yes

Missouri

Gold and silver bullion is exempt from state and local taxes as long as the metals meet certain purity requirements.

Local taxes: Yes

Montana

No state sales tax on any purchases.

Local taxes: No

Nebraska

No state sales tax on bullion. Policies remain favorable for gold, silver, platinum, and palladium into 2026 with no major changes.

Local taxes: Yes

Nevada

No sales tax on gold or silver bullion purchased as a medium of exchange.

Local taxes: Yes

New Hampshire

No statewide sales tax of any kind. You will not pay taxes on gold or silver bullion.

Local taxes: No

New Jersey

Senate Bill 721 eliminated sales tax on investment metal bullion and coins, effective January 1, 2025.

Local taxes: Yes

New Mexico

Residents pay a gross receipts tax on gold and silver purchases. The rate ranges from 5.125% to 8.8675% depending on location.

Local taxes: Yes

New York

Purchases under $1,000 are subject to a 4% state sales tax. Purchases of $1,000 or more are exempt.

Local taxes: Yes

North Carolina

Gold and silver bullion is exempt from sales tax if its value is determined primarily by metal content. This applies to coins, leaf, foil, and other forms where value is calculated on metal content.

Local taxes: Yes

North Dakota

No state sales tax on gold or silver bullion coins or bars.

Local taxes: Yes

Ohio

House Bill 110 (2021) eliminated state sales tax on precious metals.

Local taxes: Yes

Oklahoma

No state sales tax on gold or silver.

Local taxes: Yes

Oregon

No sales tax on any purchases, including precious metals.

Local taxes: No

Pennsylvania

No state sales tax on precious metals.

Local taxes: Yes

Rhode Island

No state sales tax on silver or gold bullion, whether legal tender or not.

Local taxes: Yes

South Carolina

No state sales tax on precious metals.

Local taxes: Yes

South Dakota

Most bullion coins and bars are not subject to state sales tax. When it is eventually time to liquidate, learning how to sell gold and silver tax-free can save you more than the sales tax savings on the buy.

Local taxes: Yes

Tennessee

Governor Lee signed HB 1874/SB 1857 in 2022, eliminating state sales tax on gold, silver, platinum, and palladium bullion.

Local taxes: Yes

Texas

Under Texas Tax Code § 151.336, the state exempts gold, silver, numismatic coins, platinum, and silver bullion with no minimum purchase amount.

Local taxes: Yes

Utah

No state sales tax on gold, silver, or other precious metals. Utah also offers a nonrefundable credit against state tax if you report capital gains on your federal return for U.S.-issued gold and silver coins.

Local taxes: Yes

Vermont

Vermont charges 6% sales tax on gold and silver products.

Local taxes: Yes

Virginia

Virginia exempts qualifying gold, silver, and platinum bullion and legal tender coins with no minimum purchase amount. HB 936 eliminated the threshold in 2022, and the exemption is currently in effect through June 30, 2028.

Local taxes: Yes

Washington

Under ESSB 5794, Washington’s retail sales tax applies to bullion purchases made on or after January 1, 2026. The state base rate is 6.5%, and combined state and local rates are higher and vary by location.

Local taxes: Yes

Washington, D.C.

Sales tax applies to gold and silver bullion purchases in the District.

West Virginia

No state sales tax on gold or silver.

Local taxes: Yes

Wisconsin

Governor Evers signed Assembly Bill 29, which exempts precious metals from state sales tax.

Local taxes: Yes

Wyoming

No state sales tax on precious metals per the Wyoming Legal Tender Act.

Local taxes: Yes

Specific tax considerations

Bullion coins vs. numismatic coins

States generally base their exemptions on whether a coin or bar qualifies as investment-grade bullion. Products that meet IRS standards for a Gold IRA typically fall under these exemptions. Numismatic coins, which the IRS does not permit in a retirement account, may be treated differently depending on your state.

If you are buying collectible coins, check your state’s definition of “bullion” before you purchase.

Impact of metal content

Several states only waive sales tax if your metals meet a minimum purity level. A few examples:

- Illinois: 98% purity minimum

- Minnesota: 99.9% purity minimum

- Michigan: 90% purity minimum

Most standard bullion products from reputable dealers will clear these thresholds.

Online purchases and shipping address

For online orders, sales tax is based on where the dealer ships the metals, not where your billing address is. Your billing information is used for payment verification only. If you are shipping to a different address than usual, verify the tax rules for that location before you check out.

Other tax law regulations

Capital gains taxes

Sales tax is a one-time cost at purchase. Capital gains tax applies when you sell at a profit.

At the federal level, the rate depends on how long you hold the metals. If you sell within one year of buying, gains are taxed as ordinary income. If you hold for more than one year, gains are taxed at a maximum rate of 28% because the IRS classifies precious metals as collectibles. Most states impose their own capital gains taxes on top of the federal rate.

A Gold IRA can help you reduce or defer these taxes within a retirement account structure. For long-term holders, this is worth understanding before you decide how to buy.

Selling regulations

Here is how IRS reporting works when you buy or sell gold:

- When you buy: The IRS does not track individual purchases. No automatic reporting occurs unless your gold is held inside a tax-advantaged retirement account, in which case the account custodian handles the reporting.

- When you sell: Dealers may be required to file a Form 1099-B for larger transactions. Ask your dealer about their specific thresholds.

- If you make a profit: You are responsible for reporting gains on your tax return as capital gains. This applies whether or not your dealer filed a 1099-B.

How to sell gold and silver tax-free

You can’t avoid every tax on a gold or silver sale. But you can legally reduce or eliminate most of them, depending on how you structure the purchase, the hold, and the sale itself.

Buy in a sales-tax-exempt state

As of 2026, 44 states exempt precious metals from sales tax. The six that still charge it are Hawaii, Maine, Maryland, New Mexico, Vermont, and Washington. If you live in one of those states, buying from an out-of-state dealer with no nexus in your state may allow you to skip the sales tax on your purchase, which directly protects your margins when you sell later.

For online orders, remember that sales tax is based on where the metals are shipped, not where you place the order from. That distinction matters if you’re buying across state lines.

Hold your metals inside a Self-Directed IRA

This is the most straightforward path to tax-free or tax-deferred growth. In a traditional Self-Directed IRA, your gold and silver grow without triggering capital gains until you take distributions. In a Roth Self-Directed IRA, qualified withdrawals are completely tax-free, including all the gains.

IRC §408(m) requires IRA-held bullion to meet commodity exchange fineness delivery standards and be stored with an approved custodian. The commonly cited figures, 99.5% for gold and 99.9% for silver, are COMEX standards rather than IRS-stated percentages. Products like American Gold Eagles and approved gold bars qualify under these rules.

Use the stepped-up cost basis on inherited metals

When heirs inherit physical gold or silver, the IRS resets the cost basis to the market value on the date of death. That means decades of price appreciation get wiped from the tax ledger entirely. If your parents bought gold at $400 an ounce and it’s worth $2,500 when you inherit it, your taxable gain starts at $2,500, not $400. Sell at $2,500, and you owe nothing in capital gains.

This makes gold and silver one of the more tax-efficient assets to pass between generations, especially compared to retirement accounts that create taxable events for heirs.

Offset gains with capital losses

If you’re selling gold or silver at a profit, you can pair that sale with losses from other investments to reduce or zero out the tax bill. The IRS allows capital losses to offset capital gains dollar-for-dollar. If your losses exceed your gains, you can deduct up to $3,000 per year against ordinary income and carry the rest forward to future tax years.

Know the reporting thresholds

Not every sale triggers a 1099-B from your dealer. The IRS only requires dealer reporting on specific items at specific quantities:

- Gold bars of 1 kilo or more at .995 fineness

- Silver bars of 1,000 troy ounces or more at .999 fineness

- Certain coins like Gold Maple Leafs or Krugerrands in lots of 25 or more

American Gold Eagles and American Silver Eagles are exempt from 1099-B reporting entirely, regardless of quantity. This does not eliminate your tax obligation, but it does mean smaller, strategic sales of certain products stay between you and your tax return.

Watch for state-level capital gains exemptions

A handful of states are moving to exempt precious metals gains from state income tax altogether. Missouri eliminated state capital gains tax on gold and silver sales as of January 1, 2025. Iowa did the same under House File 659 in 2024. Other states are considering similar legislation.

If your state follows suit, federal capital gains (taxed at the 28% collectibles rate for metals held over a year) would be your only obligation.

Sound money and economic impact

Gold and silver have served as a store of value for centuries because their worth is tied to a physical asset. That is part of why many state legislatures have removed sales tax barriers on precious metals, treating them as investments rather than consumer goods.

Organizations like the Sound Money Defense League have worked state by state to expand these exemptions. Their argument is that taxing gold and silver discourages citizens from holding real assets outside the banking system. As of 2026, most states have accepted this reasoning.

Maryland and Washington are the recent exceptions. Both added new taxes on bullion in 2025 and 2026, respectively, which puts them out of step with a broader national trend toward exemption.

Final thoughts on sales tax on gold and silver

For most buyers, some form of tax applies to a gold or silver purchase. State-level sales tax applies in six states plus D.C., local taxes apply across most of the rest, and only five states charge nothing at all.

To learn more about investing in gold, silver, or other precious metals, connect with the Swiss America team today!

Sales tax on gold and silver by state: FAQs

Is gold taxable in the USA?

In most cases, yes. You may owe sales tax when you buy and capital gains tax when you sell at a profit. Only Alaska, Delaware, Montana, New Hampshire, and Oregon have no sales tax at all, and the IRS taxes long-term gains on gold as a collectible at a maximum rate of 28%. Metals held inside a Self-Directed IRA grow tax-deferred, or tax-free in a Roth, until you take distributions.

How much silver can I buy without reporting?

Any amount. As a buyer, you have no obligation to report silver purchases to the IRS, because the reporting duty falls on the dealer. Dealers file a Form 1099-B only on specific transaction types, such as silver bars of 1,000 troy ounces or more at .999 fineness on the sell side. American Silver Eagles are exempt from 1099-B reporting entirely, no matter how many you buy.

Do I pay sales tax on gold bought online?

It depends on the ship-to state. Sales tax on an online order is based on where the dealer ships the metals, not your billing address. If the metals ship to one of the six states that still tax bullion, you will owe it, and local taxes may apply almost everywhere outside Alaska, Delaware, Montana, New Hampshire, and Oregon.

Is buying gold reported to the IRS?

No. The IRS does not track individual gold purchases, and no automatic reporting occurs when you buy, unless the gold is held inside a tax-advantaged retirement account where the custodian handles reporting. Reporting can apply when you sell, where dealers may file a Form 1099-B for larger transactions above set thresholds.

Which state is best to buy gold and silver in?

Alaska, Delaware, Montana, New Hampshire, or Oregon. These five charge no sales tax at either the state or local level, so your purchase carries no added tax cost. Buyers elsewhere can still avoid state sales tax in the 44 states that exempt bullion, though local county or city taxes may apply.

The information in this post is for informational purposes only and should not be considered tax or legal advice. Please consult with your own tax professionals before making any decisions or taking action based on this information.